Karl explains how we capture lending, borrowing, repo and collateral exclusion/inclusion criteria for you automatically...

For many of us working in financial compliance, particularly in the complex area of shareholding disclosure, we find that having navigated the complexities of interpreting rules from dozens of countries where our firm might have an interest, yet another wrinkle in the goal of exacting the correct calculations and percentages appears: lending, borrowing, repo and collateral assets!

These terms alone are enough to make one shudder, let alone the thought of considering how each of these so-called “securities financing transactions” affect compliance results.

On both the buy and sell side, we find that even the initial task of gathering the appropriate data from stock lending programs, repo, and prime broker activity is daunting. Despite this, regulators from around the world have recently brought this area into focus in passing regulations. Consider the European Union’s “Securities Financing Transactions Regulation” (SFTR), which comes into force on January 1st, 2018. Where such data wasn’t required previously, it now requires that a host of information related to lending, borrowing, repo and other securities financing transactions be provided.

At FundApps, we’ve analysed over 90 jurisdictions, captured the regulatory requirements in our rules engine, and clarified the data required to ensure that all of these transactions are captured in regard to shareholding disclosure. Unlike the European SFTR, we don’t need anything close to the amount of data required to ensure the accurate reporting for shareholding disclosure obligations.

Tracking the important features of the legal agreements governing these transactions can be an important factor.

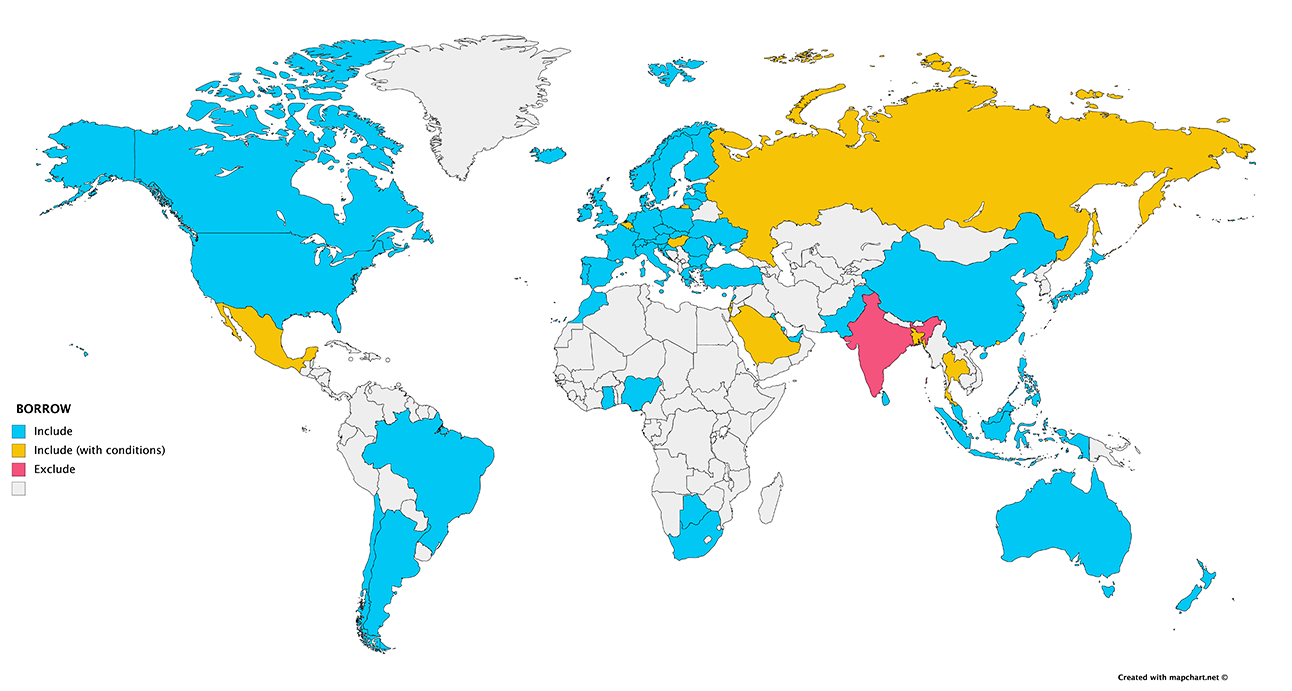

Whether lent, borrowed, or collateral (taken or given) should be included or excluded VARIES depending on the country and regime! The regulation in each country needs to be analysed individually to determine whether the regime requires one to exclude or include these holdings.

Very few generalisations can be made.

Securities lending agreements are standardised, but there can be differences and attributes of them that have to be confirmed.

Repurchase (repo) agreements or other agreements covering the collateral desk can have different terms.

The analysis of inclusion/ exclusion of securities financing transactions turn on whether the legal agreements covering such activity include certain features such as:

- Does the activity include the legal transfer of title?

- Has the power to exercise voting rights been transferred?

If lending activity reduces one’s disclosable amount and would cause a percentage holding to pass through a disclosable threshold, failing to exclude lent would mean one would not fulfil all disclosure requirements.

In the EU, lending is treated as a disclosable event if the lending (considered a “change in nature of holding”) would cause one’s percentage to pass through a threshold in either the “shares” or “financial instruments” buckets.

Failing to include (or exclude) borrowed securities could lead to a missed disclosure in many jurisdictions.

Many financial services companies hold information related to borrowings separately from their position and static data.

Failing to include stock borrowings could mean a disclosure is missed if that borrowed amount could tip one’s calculated percentage holding over the threshold.

To learn more about how we capture lending, borrowing, repo and collateral exclusion/inclusion criteria for you automatically Book a demo or contact us to learn more.