Obligations and Sanctions.

In 2016 we published a whitepaper on Shareholding Disclosure in Sweden, because at that time the regulations had caught a lot of companies out. Unlike many regulatory authorities around the world, theSwedish Financial Supervisory Authority (the FI for short) had made their data on Short Selling and Major Shareholding filings and fines publicly available.

Since then the whitepaper has helped several of our clients to model financial risk and build the internal business case for the need to automate their compliance requirements. For example, sourcing concrete information on fines received for neglecting disclosure obligations or takeovers is not easy. Here, we take a look at this data again and summarise the trends in the sanctions meted out by the FI. For an even more in-depth insight, please see our whitepaper on the subject.

Background on Swedish Regulation

The Shareholding Disclosure obligation in Sweden stems from the Financial Instruments Trading Act. This states that the lowest threshold for which a disclosure obligation is triggered is when an investor owns 5% or more of the total outstanding shares, or total voting rights, of a company. Any changes which result in their holdings crossing 10%, 15%, 20%, 25%, 30%, 50%, 66.6% and 90% will trigger further disclosures.

As a member of the EU, Sweden inherits its short selling regulation from the European Parliament’s Regulation 236/2012 Article 12. These regulations stipulate that in order to short sell, the sale needs to be covered. This means that the seller must make arrangements to ensure that at settlement they will have the shares available. In addition, short positions must be disclosed if they reach 0.2% of the issued share capital of the company concerned, and each 0.1% below that position.

We analysed a dataset of filings data in Sweden from November 2012 until August 2016. This includes monetary fine data from September 2010 until August 2016. It consists of approximately 700 unique market participants, 7000 compliant disclosure filings and 150 fines.

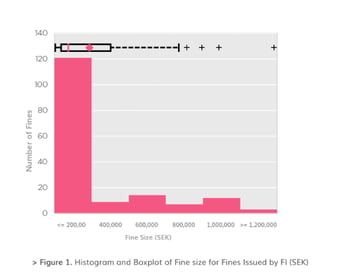

Fines in Sweden

An analysis of our dataset showed that the overwhelming majority of fines lie between 0-200,000 SEK (equivalent to almost £16,000 or $21,000). However, we also found that much larger fines that would be considered outliers in smaller sample sizes are unexpectedly common.

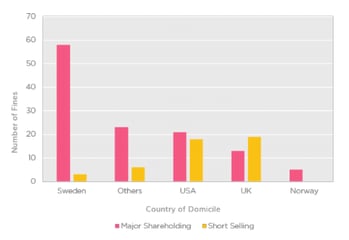

The diagrams below strongly suggest that UK and US domiciled companies are much more likely to be fined for short selling disclosure obligation contraventions than Swedish-domiciled ones.

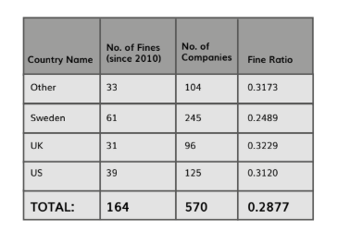

We can see that Sweden has a lower fine-to-company ratio, with roughly 1 in every 4 companies being fined during the time period that we are looking at. This increases to almost 1 fine per every 3 non-Swedish companies participating in this market. This indicates that companies are less familiar with restrictions outside of their local jurisdiction, and are statistically more likely to disclose inaccurately, or not on time.

Conclusion

Swedish shareholding disclosure regulations go beyond the minimums stipulated in the Transparency Directive. Investors not intimately familiar with all the details of the legislation may find themselves unaware of disclosure obligations, and therefore may end up with unexpected fines. Fines of up to $260,000 (2,550,000 SEK) are not uncommon, as Mawer Investment Manager discovered just a few months ago.

If you are interested in a more in-depth look into Shareholding Disclosure in Sweden then please download our whitepaper here.