One of the most misunderstood aspects of compliance with Shareholding Disclosure and transparency regulation is determining which entities, funds, or portfolios one must aggregate to know one’s ownership of a company or class of security.

It is common for most countries with a regulated stock market to impose requirements on holders of securities to disclose when their holdings reach certain percentage thresholds, for example 5, 10, 15, and 20%. At first glance, those percentages might seem high, particularly for an asset manager focused on a particular set of portfolios or an investment management company in a specific region.

However, in almost every jurisdiction, there are specific requirements to aggregate portfolios of assets across the management entities of a global bank, a holding company of an asset manager, or the controlling entity/persons of hedge funds. In fact, many countries require aggregation all the way to the top level holding company. This means that it is critical to obtain the complete set of assets and a raft of security data ACROSS all divisions of a financial institution in order to comply with regulations.

Failing to do so is very risky financially as penalties and sanctions can be levied for non-disclosure, as well as being risky reputationally given that many sanctions are made public or must be noted explicitly on company marketing material (depending on the jurisdiction).

Although we can identify commonalities among countries like the requirement to combine all assets and calculate one’s holding at the top-level holding company, there are enough differences between countries to warrant special attention and nuanced monitoring for each market. At a high level, let’s conceptualise these differences in two categories: (1) aggregation level and (2) aggregation type.

Aggregation Level:

For a given jurisdiction, disclosure obligations that kick in once a holder has crossed a threshold (e.g. 5%) can be interpreted to apply at:

1. The level of the investment manager (the legal entity contracted with discretionary management over assets)

2. The level of the investment manager and its “controlling entities” (above it in the corporate tree)

3. The level of the top-level holding company

4. A combination of all entities listed above

We are not done discussing the levels at which one must aggregate holdings, but so far, one can imagine how many combinations of calculations would be required, depending on the corporate hierarchy (and we’ve seen some interesting ones!).

In addition to the entities described above, one must assess another grouping of assets that is relevant and varied by country: fund or portfolio level.

What if a UCITS fund, hedge fund, mutual fund, or another collective investment scheme crosses a threshold (and some thresholds are much lower than 5%) on its own? Does that trigger a disclosure requirement? In many cases it does, but it depends on the regulatory regime in a given country. Some regulators want holders to disclose at portfolio or fund level and some do not. The requirement might even depend if there is a legal personality attached to the fund.

What if there are investment fund series, commingled funds or UCITS umbrella funds involved? The requirement to aggregate and calculate a result at the umbrella or total series level might be required.

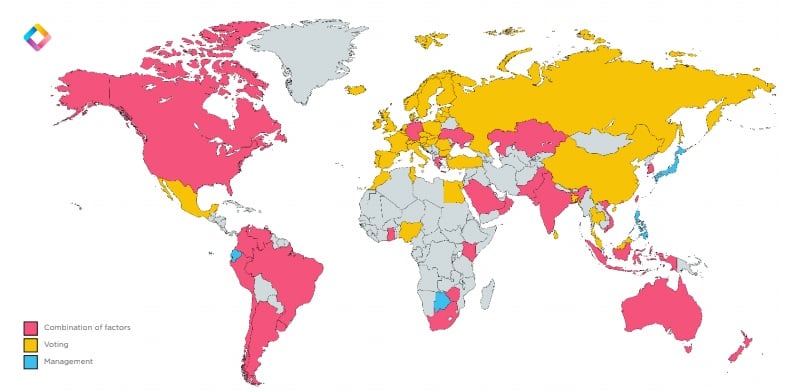

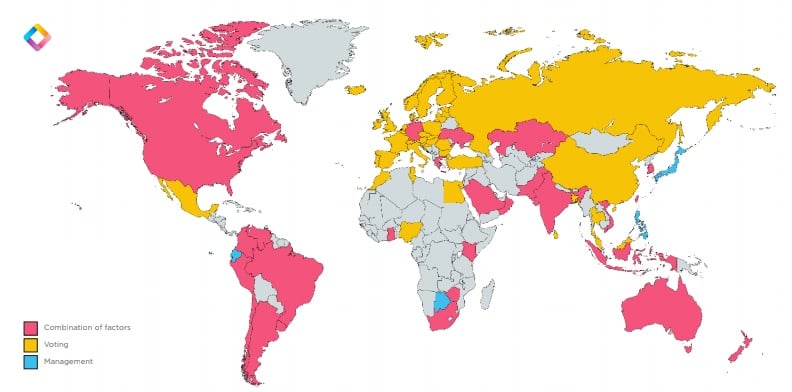

Aggregation Type:

The interpretation of disclosure regulation in each country requires one to not only to identify which assets to combine up the corporate tree, but also to know what relationship each entity has with the assets it holds, manages, or votes.

By implementing the EU Transparency Directive, the countries in the EU must, at a minimum be interested in which entities hold power over the voting rights of the securities (or the reference securities of derivatives) they manage, hold, or own. Even if an investment manager has discretionary management authority, they may not have such authority for every portfolio they manage. Immediately we see how accurate calculations of holdings must include the variable of who holds the power to vote attached to shares. There are many other countries for which the power over voting rights is the main component of deciding which assets to aggregate and what entities to aggregate them to.

Other countries are primarily concerned with who has discretion over the management of assets or the power to buy/sell securities (usually on behalf of another party). There are cases where although one might be the ultimate beneficial owner of assets, the disclosure obligation has been shifted to the party who has discretion over the management of assets.

For other countries, the concern might not be with the power over voting rights, or management power, but in the actual legal owner (legal title holder) or the ultimate beneficial owner.

Ensuring that a clear interpretive judgement is made in regards to each entity’s relationship to the assets they hold or manage is critical.

Including certain holders, or omitting others based on a flawed understanding of their role, will likely mean incorrect disclosure calculations and the potential for hefty fines.

It is crucial that your firm’s corporate tree is modeled precisely among the primary dimensions of aggregation level and type. It is a complicated and important step in complying with Shareholding reporting obligations and one that is made easier with an expert compliance team and cloud software that ensures regulatory changes over time, including those in the area of aggregation are done correctly.