After the tightening of EU regulations around foreign investments and the introduction of Foreign Investment Risk Review Modernization Act (FIRRMA) in the US, Japan unveiled its new streamlined “Foreign Exchange and Foreign Trade Act'' (FEFTA) in an effort to promote foreign direct investment (FDI) whilst protecting national interest.

Click below to hear our Sales Manager, Brittany May, explain what this regulation means and how FundApps can help (hint: we've got this rule update covered!). Or, read on for an overview.

Within FEFTA foreign investors in Japan are divided into three categories: foreign financial institutions, general investors (including sovereign wealth funds and pension funds) and investors sanctioned under FEFTA, or State-owned enterprises. Each of these investor types has its own disclosure requirements depending on the issuer.

Every listed issuer in Japan falls within one of three categories and these are:

- Category 1 - Companies subject to post-investment report only (i.e. non-designated business sectors);

- Category 2 - Companies conducting business activities only in the designated business sectors other than core sectors; or

- Category 3 - Companies conducting business activities in the core sectors

This is where it gets a little complicated. Grab a coffee ☕ and get comfortable as we go through this update on Japan’s FDI regime.

Foreign financial institutions only have to disclose if they acquire 10% of the voting rights or issued share capital of any listed issuer, regardless of sector as long as the exemptions are complied with.

It gets more interesting when looking at general investors as the disclosure requirements vary on how the issuer is defined:

- If the issuer is category 1, a 10% disclosure is required

- If the issuer is category 2, disclosure is required at 1%, 3% and 10% and any increases above 10%

- If the issuer is category 3 disclosure is required at 1%, 3% and 10% and any increases above 10%, additionally, pre-approval is also required from 10% and any subsequent increases.

It’s worth noting, that the 1% and 3% disclosures are only required the first time the threshold is crossed upwards.

Finally, Investors sanctioned under FEFTA, or State-owned enterprises are required to seek pre-approval and disclose any changes at 1% and above.

If this is the streamlined version, reading the previous legislation must have been like splitting the atom.

We have seen changes across the globe due to COVID-19, where regulations have tightened up in order to protect national security interests, however, these are all temporary when compared with Japan. It appears that while other countries have “moved in” with regulations, Japan has decided to “propose” showing a commitment to growing and strengthening their economy. This can be considered against the norm when it comes to sensitive industry regimes, however, we will wait and see if others take the plunge and buy that ring.

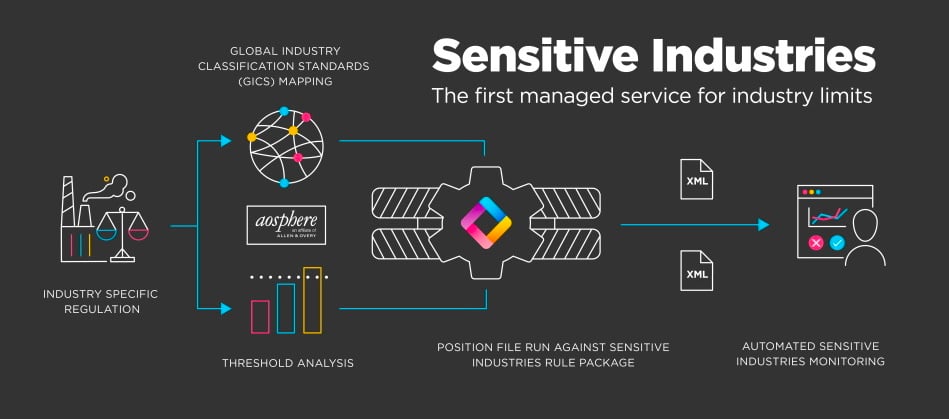

FundApps covers the FEFTA regulation as part of its Sensitive Industries service, automating alerts for compliance professionals who are subject to industry specific investment restrictions, which apply in almost every major jurisdiction across the globe. Want to see our service in action? Then get in touch!