Shareholding Disclosure Monitoring

Automate your monitoring and get ahead of disclosure requirements in over 100+ jurisdictions.

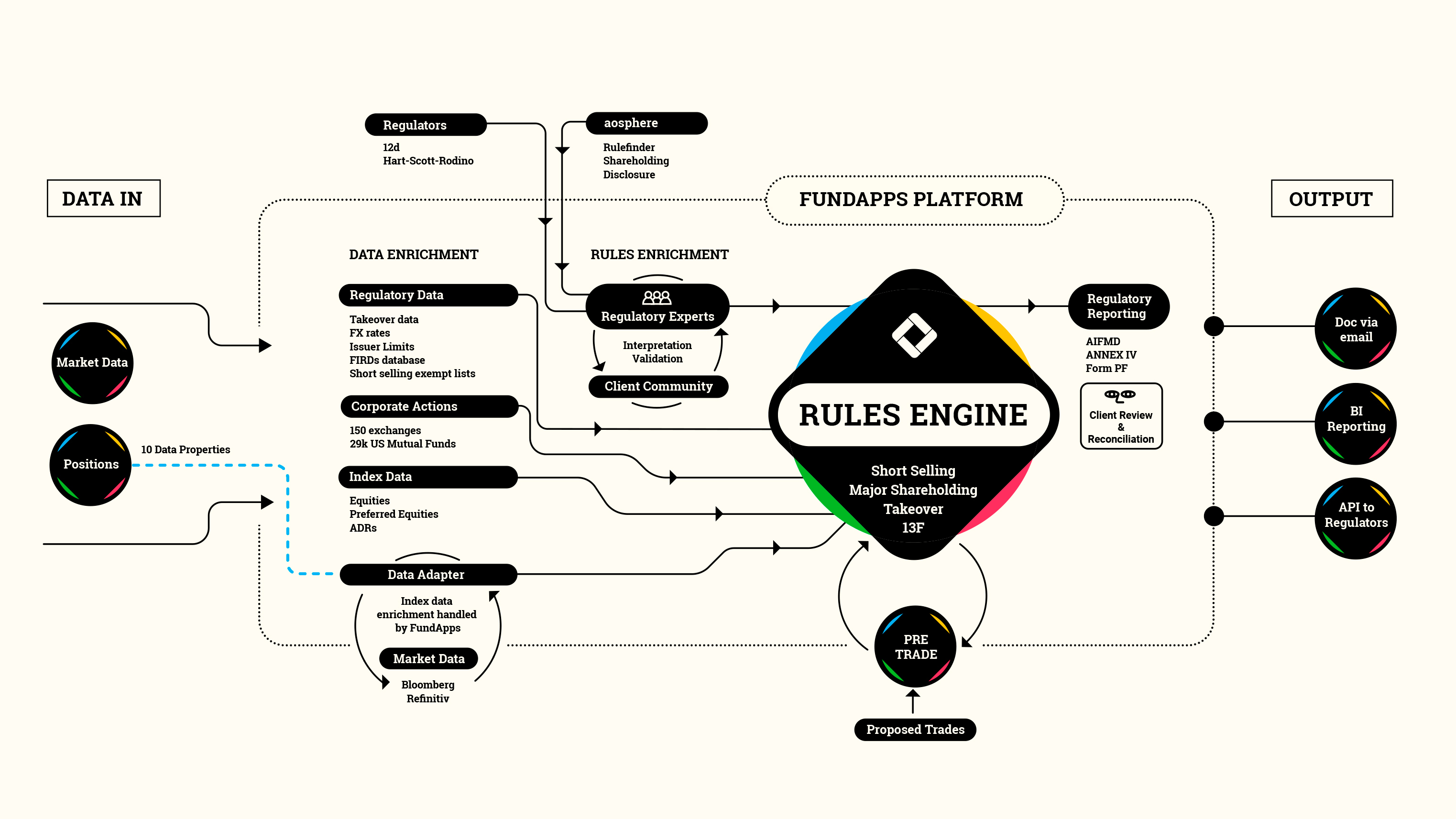

Consolidated data

Takeover panel information, short selling lists, FIRDS information and issuer-specific data is automatically sourced making data accessible and usable.

Rule coverage

Our in-house regulatory experts take aosphere's legal and regulatory interpretation and code them into a single set of always up-to-date rules used by all our clients.

Results dashboard

Focus efforts where it counts by using our concise daily summary of what needs to be done and what's to come including custom rule alerts and access to historical data.

Aggregation

Comply with shareholding disclosure by correctly aggregating positions at entity to portfolio level, as well as by ownership type (legal, voting, management).

Add-on: Pre-Trade Disclosure API

Need to check thresholds before trading? Our Pre-Trade API helps you stay compliant by assessing real-time exposure against jurisdictional limits, especially useful for high-volume or sensitive trades.

…I can highly recommend their people and solution to any firm, large or small, which deals with shareholding disclosures. At FundApps the team is always ready to go the extra mile to fit your need. More importantly, they will think with you. My experience with them has been nothing but EXCELLENT!

FundApps has allowed our organisation to stay on top of time sensitive disclosure requirements, alert us to approaching threshold breaches, accommodate rule changes in jurisdictions across the globe and provide audit trails on historical disclosures...

FundApps has simplified the complexities of shareholding disclosure regulations into one intuitive, easy to use platform and provides continued support from both their customer success team and content team when required.

...With the help of FundApps, we can commit to delivering high-quality investment outcomes to our clients. We're excited about joining FundApps’ compliance community and we look forward to working together.

FundApps’ Shareholding Disclosure service provides an intuitive and transparent solution to the ever-changing regulatory requirements we face. It will enhance our confidence in the filings we make, the integrity of the data used and the auditability of our shareholding disclosure reporting.

The combination of the Rule Commentary functionality, the explanation from FundApps and the detail provided about the rules from aosphere provides our business with a reliable solution that we can continue to use as our business grows.

...Using FundApps Filing Manager, my disclosures are ready to be submitted directly to the regulator at the simple click of a button. Once completed, I can view the filing status in one place with an entire audit trail, eliminating the need to cross-check various sources and validate the information submitted, making the entire disclosure process seamless.

Why 'data-only' Shareholding Disclosure fails the defensibility test

A data-only approach leaves shareholding disclosure exposed to defensibility gaps. Here’s why data alone won’t stand up to scrutiny.

How a ‘Data-Only’ approach compromises shareholding disclosure from the start

Shareholding disclosure compliance needs more than data feeds. Learn how jurisdiction rules, instruments, and workflows shape accurate, scalable monitoring.

Regulation in motion: Looking back at 2025 and preparing for 2026

A view on global regulation in 2026, covering SEC priorities, geopolitical risk, AI governance, and how compliance teams can prepare for rising complexity.